A single hyperscale data center can consume 50,000 tonnes of copper. The world’s mines can barely keep up with current demand. Ore grades have fallen 40 percent since 1991. And the companies building the AI future are now outbidding entire national power grids for the metal that makes it all possible.

By The Index Today Staff · May 20, 2026 · Commodities · 10 min read

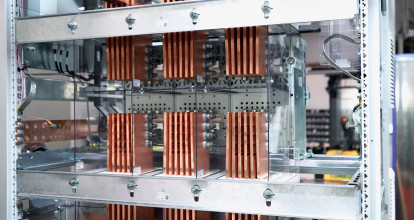

Somewhere in central Texas, a concrete slab the size of several football fields is being prepared for one of the largest AI data centers ever built. The facility, when completed, will house tens of thousands of GPUs running machine learning workloads around the clock. It will consume more electricity than a small city. And it will require, by conservative estimates, up to 50,000 tonnes of copper — for power distribution, cooling infrastructure, high-density cabling, grounding systems, and the transformers that connect the campus to the grid.

That single facility represents more copper than some mid-sized mines produce in an entire year.

Now multiply it. Microsoft, Google, Amazon, and Meta are collectively spending an estimated $725 billion on data center capital expenditure in 2026 alone — a 77 percent increase over last year. OpenAI’s $500 billion Stargate initiative is ramping up alongside dozens of similar projects across the United States, Europe, and Asia. Each one needs copper at a scale that the mining industry was never designed to deliver. And the problem is not theoretical. It is happening now.

Spot copper prices exceeded $14,000 per tonne at the beginning of 2026, touching record highs. JPMorgan expects prices to reach $12,500 per tonne in the second quarter of 2026, averaging around $12,075 for the full year. UBS projects $13,000 by year-end. Citi analysts have forecast $15,000 by mid-year. The range of estimates varies, but the direction is unanimous: higher, and for structural reasons that have nothing to do with speculation.

The red metal — once a reliable but unglamorous industrial commodity — has become the physical bottleneck of the AI revolution. And the supply math is getting worse.

The Demand Problem

Copper has always been essential to the modern world. It conducts electricity better than any affordable alternative. It is embedded in every power line, every electric motor, every circuit board. But three converging forces are now pushing demand into territory that the industry has never confronted simultaneously.

The first is AI. Data centers currently consume about 1.5 percent of global electricity supply — roughly equivalent to the entire United Kingdom. The International Energy Agency projects that figure will more than double by 2030, with artificial intelligence responsible for the majority of the increase. An AI-optimized data center uses up to three times more copper than a traditional facility of equivalent size, owing to the denser power requirements, more complex cooling systems, and higher-capacity wiring. Red Cloud Securities estimates that data centers could consume as much as 10 percent of North American electricity within five years, with individual hyperscale facilities requiring staggering quantities of the metal.

The hyperscalers are not merely buying copper at scale. They are locking in long-term supply agreements that remove inventory from the open market, leaving traditional buyers — utilities, grid operators, manufacturers — scrambling for what remains. As one Wood Mackenzie analyst told the Financial Times, the hyperscalers are “outbidding grid suppliers on things like transformer units.” The irony is acute: the power grid that these data centers depend on is being starved of the very materials it needs to expand — by the data centers themselves.

The second force is electrification. The energy transition — electric vehicles, wind turbines, solar installations, battery storage systems, grid expansion — is copper-intensive at every level. An electric vehicle contains three to four times more copper than a conventional internal combustion engine vehicle. BloombergNEF projects copper consumption from power transmission and wind energy alone to nearly double by 2035. Battery energy storage systems are rivaling EV batteries in demand growth, with China adding storage capacity at record pace.

The third force is urbanization and infrastructure development across the Global South, where rising living standards and expanding electricity access are driving steady, structural growth in copper consumption that receives less attention than AI or EVs but is no less consequential.

Layer these demand curves on top of one another, and the supply math becomes, as S&P Global’s Daniel Yergin put it, a “systemic risk for global industries, technological advancement, and economic growth.”

The Supply Problem

The supply side offers no relief. Ore grades at legacy mines have fallen by roughly 40 percent since 1991, meaning that producers must move more earth to extract less metal. The average lead time from discovery to production for a new copper mine is 15 to 20 years — a timeline that renders current exploration irrelevant to current demand. Permitting battles in Chile, Peru, and the United States have delayed or killed major projects. Environmental and community opposition has intensified.

Then there are the unplanned disruptions. Indonesia’s Grasberg mine — one of the world’s largest — has been offline through much of 2026. The Kamoa-Kakula complex in the Democratic Republic of the Congo has faced its own operational challenges. These are not marginal producers; they are pillars of global supply, and their absence tightens a market that was already stretched.

The International Energy Agency’s latest critical minerals outlook places copper on a path where existing and planned mines meet only about 70 percent of projected 2035 demand. Wood Mackenzie estimates that a refined-copper deficit of 304,000 tonnes materialized in 2025, with a wider gap expected this year. The International Copper Study Group projects the market shifting from a slight surplus in 2025 to a deficit exceeding 150,000 tonnes in 2026. Some analyses project a cumulative deficit of 10 million metric tonnes by 2040.

Recycling provides some buffer — roughly 30 percent of global copper demand is currently met through secondary supply — but it cannot scale fast enough to close the gap. And the geographic concentration of smelting and refining capacity in China, which controls 40 to 50 percent of global processing, introduces its own supply chain risk in an era of trade wars and export controls.

The Price Signal

Commodity markets exist to solve supply-demand imbalances through price. When copper hits $14,000 per tonne, the market is sending a message: find more copper, or find something else. But for most applications, there is no something else. Aluminum can substitute in some wiring contexts, but at significant efficiency losses. Fiber optics handle data transmission, not power distribution. The data centers, the EVs, the grids — they need copper. The demand is, in the language of economists, non-discretionary.

What this means in practice is that prices must rise high enough to incentivize new mine development — a process that takes years — while simultaneously rationing current supply among competing demands. Goldman Sachs has suggested that prices may need to reach $15,000 per tonne to trigger sufficient long-term investment. In the interim, the market will allocate copper to whoever is willing to pay the most, which increasingly means the hyperscalers with the deepest pockets.

The distributional consequences are significant. Developing countries building electricity grids cannot compete with trillion-dollar technology companies for copper supply. Renewable energy projects operating on thin margins may be priced out. The energy transition, which depends on massive copper deployment, could be slowed by the very commodity it requires.

What Comes Next

Copper sits at the center of a collision between the world’s most powerful trends: artificial intelligence, electrification, urbanization, and resource scarcity. The bull case is straightforward and, at this point, close to consensus: demand is rising faster than supply can respond, and the deficit will widen before it narrows. The only questions are how high prices go and how the consequences are distributed.

For investors, copper has become one of the most compelling structural trades in commodity markets — a bet on physical scarcity that is driven by secular demand growth rather than cyclical speculation. For policymakers, it is a warning: the energy transition and the AI revolution both depend on a metal that the world does not produce enough of, and the gap is growing.

For the rest of us, it is a reminder that the digital future is built on physical materials, extracted from the earth by miners, shipped on freighters, and refined in smelters. The cloud is not weightless. The algorithm is not immaterial. And the price of copper — unglamorous, essential, increasingly expensive — is the number that tells you what the future actually costs.