Brent crude surged 55 percent. Twenty thousand seafarers are stranded on two thousand ships. Fertilizer prices are doubling. And the Strait that carries a fifth of the world’s oil remains, for all practical purposes, closed. Three months into the Iran war, the commodity shock is no longer a disruption — it is a restructuring.

By The Index Today Staff · May 20, 2026 · Commodities · 12 min read

On the morning of March 4, an official from Iran’s Islamic Revolutionary Guard Corps made an announcement that would ricochet through every trading floor, shipping office, and government ministry on earth. “The Strait is closed,” he said. “If anyone tries to pass, the heroes of the Revolutionary Guards and the regular navy will set those ships ablaze.”

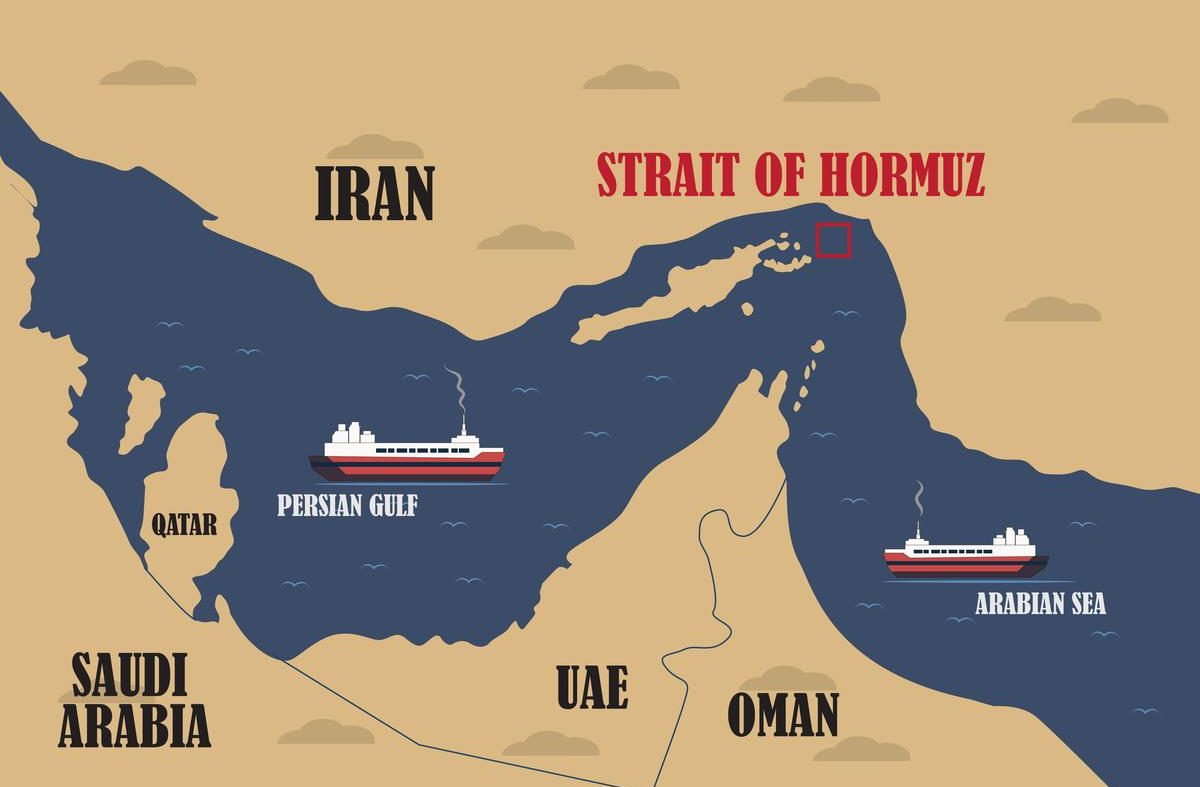

Within hours, tanker traffic in the Strait of Hormuz — the narrow waterway between Iran and Oman through which roughly 27 percent of the world’s maritime crude oil and petroleum products pass — had effectively ceased. Within days, Brent crude had blown past $100 a barrel. Within weeks, the International Energy Agency had characterized the disruption as “the largest supply disruption in the history of the global oil market.” Its head went further, calling it “the greatest global energy security challenge in history.”

Now, nearly three months later, the Strait remains functionally closed. The ceasefire announced on April 8 briefly lowered prices and raised hopes, but it collapsed within days when Iran reimposed control over the waterway, with reports of gunfire on tankers and commercial vessels turning back. As of mid-May, Brent crude is trading above $107 a barrel — more than 45 percent higher than pre-war levels — and the cascading consequences extend far beyond energy.

This is the story of a commodity shock that has touched every corner of the global economy — from the fertilizer that feeds crops in South Asia to the jet fuel that moves aircraft across North America, from the cooking gas that reaches Indian households to the sulfur that underpins industrial production worldwide.

The Price Shock

The numbers trace the arc of a crisis that arrived in waves. When the U.S.-Israeli military campaign against Iran began on February 28, Brent crude stood at approximately $72 a barrel. By March 2, it had surged 10 to 13 percent to around $80-82. When Iran declared the Strait closed on March 4 and began enforcing the blockade, prices accelerated violently. By March 27, Brent had hit $112.57 — a 55 percent increase in less than a month and one of the largest single-month oil price surges on record.

The peak came shortly after, when Brent briefly touched nearly $120 a barrel. Gulf oil production had dropped by at least 10 million barrels per day as Kuwait, Iraq, Saudi Arabia, and the UAE found their export routes severed. QatarEnergy declared force majeure on all LNG contracts and began shutting down gas liquefaction facilities as tankers could not leave the Gulf. The maritime blockade was not merely disrupting trade — it was physically stranding the infrastructure of global energy commerce.

Since then, prices have oscillated between $95 and $115, driven by a cycle of ceasefire hopes, diplomatic breakdowns, and sporadic violence. Iran’s Foreign Minister declared the Strait “fully open” on April 17, sending crude prices down more than 10 percent in a single session. Three days later, the U.S. Navy fired on and seized an Iranian container ship, and Iran reimposed restrictions within hours. Trump called the move a “total violation” and renewed threats to strike Iranian infrastructure. Vice President Vance led a negotiating team to Islamabad. The talks produced nothing.

The current state is what one former U.S. energy adviser described as “no war, no oil, no straits” — a frozen conflict that satisfies no one and resolves nothing, while the global economy absorbs the cost.

The Cascading Effects

What makes this crisis fundamentally different from previous oil shocks is the breadth of its impact. The Strait of Hormuz is not merely an oil corridor. It is a chokepoint for liquefied natural gas, sulfur, fertilizer inputs, helium, and a vast range of industrial commodities that underpin supply chains across the world.

Sulfur has been among the most acutely affected commodities. Gulf countries account for roughly 45 percent of global sulfur supply, and the near-total halt of Hormuz traffic has caused sulfuric acid prices to spike. The downstream consequences reach directly into agriculture: sulfur is essential to fertilizer production, and the disruption has arrived at the worst possible moment — the Northern Hemisphere’s spring planting season.

Nitrogen fertilizer prices are projected to roughly double from 2024 levels. Phosphate prices could increase by approximately 50 percent. Data from Kpler shows that Asian nations are heavily dependent on Middle Eastern supply, receiving 35 percent of urea, 53 percent of sulfur, and 64 percent of ammonia exports from the region. Analysts warn that if supply constraints persist through the growing season, the result will be decreased fertilizer usage, lower crop yields for staple grains including wheat, rice, and maize, and food price inflation that hits the world’s poorest populations hardest.

In the United States, gasoline prices have risen by $1.16 per gallon since the war began, with the national average reaching $4.10. Jet fuel in North America has spiked 95 percent, forcing airlines to raise checked baggage fees and prompting shipping companies including the U.S. Postal Service, Amazon, and FedEx to implement fuel surcharges. Spirit Airlines ceased all operations in early May, citing unsustainable fuel costs. The irony is that the United States, as a net energy exporter, benefits from surging prices — American crude and petroleum product exports rose to nearly 12.9 million barrels per day in late April — even as its consumers bear the inflationary burden.

War risk insurance has compounded the disruption. Premiums for ships transiting the Gulf have increased four- to fivefold. When policies can be obtained at all, they carry 72-hour cancellation clauses that allow insurers to pull coverage at the first sign of escalation. Trump announced on March 3 that the U.S. government would provide political risk insurance to “all maritime trade” and offered Navy escorts for commercial vessels, but the commercial shipping industry has been reluctant to test the offer. Despite the president’s announcement of “Project Freedom” to guide vessels through the Strait, only two U.S.-flagged merchant ships made the transit in the immediate aftermath. The International Maritime Organization reports that approximately 20,000 seafarers remain stranded on some 2,000 vessels in the Strait — a humanitarian situation the IMO says has “no precedent in the modern age.”

The Structural Shift

Behind the price volatility lies a deeper question: what happens to the architecture of global energy trade when the world’s most important chokepoint proves that it can, in fact, be closed?

The Minneapolis Federal Reserve offered one of the most sober assessments. Economist Neil Mehrotra cautioned against reading too much optimism into the futures curve, where prices for future delivery fall back toward more familiar levels. The “backwardation” — higher prices for immediate delivery, lower for later months — mostly reflects extreme near-term need, not genuine market confidence in a resolution. The hole in global inventories is estimated at approximately one billion barrels of lost production — roughly two percent of annual global output. That deficit will take months to refill even after the Strait reopens.

Saudi Aramco CEO Amin Nasser was blunter. “If the Strait of Hormuz opens today, it will still take months for the market to rebalance,” he told investors in May. “If its opening is delayed by a few more weeks, then normalization will last into 2027.”

The longer-term consequences may be more significant than the immediate price shock. Resource nationalism is accelerating. Countries are reassessing their dependence on Middle Eastern supply and on chokepoints that can be weaponized. India is stockpiling strategic reserves and signing bilateral deals with the UAE. Indonesia is importing Russian crude in defiance of U.S. sanctions, citing national energy security. China is doubling down on coal — dirtier, but domestically available and free from maritime risk. The calculus that nations face is stark: should they rely on LNG from Qatar that must pass through Hormuz, or on coal that can be sourced from multiple locations?

The Iran war has not created these dynamics. It has accelerated them. And the commodity markets are pricing in not just the current disruption, but the possibility that the era of uncontested maritime energy commerce — the background assumption on which the entire postwar trading system was built — may be drawing to a close.