Oil exporters are flush. Oil importers are burning reserves. Fertilizer-dependent economies are facing food inflation that no interest rate can fix. And the currencies of a dozen developing nations are under more pressure than at any point since the pandemic. This is the crisis that the global financial safety net was built for — and it may not be enough.

By The Index Today Staff · May 20, 2026 · Currency · 10 min read

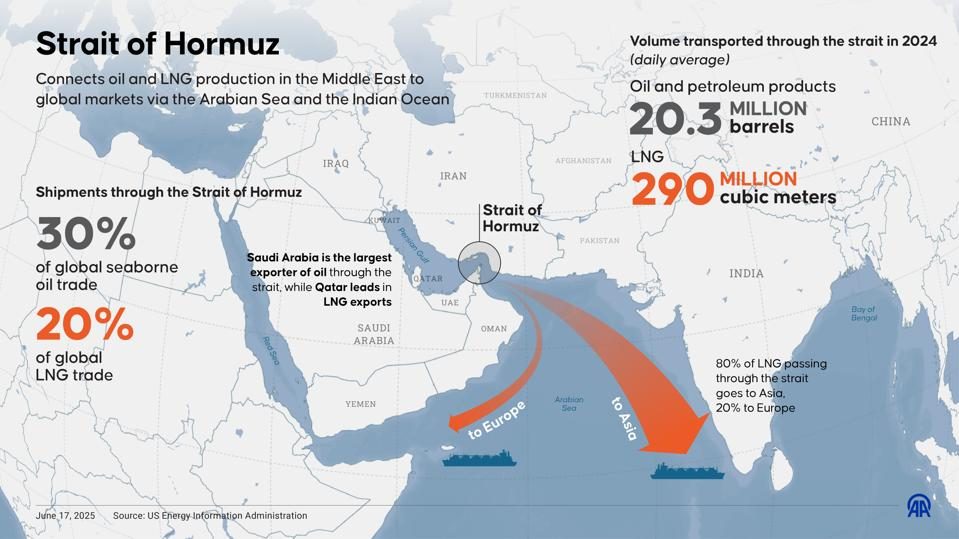

In the three months since the Iran war disrupted the Strait of Hormuz, the world’s emerging market currencies have done something they rarely do: they have stopped moving as a group. The Brazilian real is up. The Pakistani rupee is in freefall. The Indonesian rupiah is holding steady while the Bangladeshi taka is under severe pressure. The Nigerian naira is weakening, but the Saudi riyal — pegged to a dollar that its government can afford to defend — remains anchored. The Indian rupee has depreciated modestly, but the Vietnamese dong has come under sustained attack.

The familiar narrative of emerging markets — that they rise and fall together, driven by the dollar cycle, the Federal Reserve’s rate decisions, and the risk appetite of global investors — has been replaced by something more granular and more consequential. The Hormuz crisis has split the developing world along a single axis: energy. Countries that export oil and gas are experiencing windfall revenues, current account surpluses, and currency stability. Countries that import them are burning through foreign exchange reserves, running wider trade deficits, and watching their currencies weaken at exactly the moment when imported inflation — in fuel, in fertilizer, in food — is hitting their populations hardest.

This divergence is not a temporary dislocation. It is a structural repricing of risk that is being read, in real time, by every currency trader, sovereign bond investor, and IMF desk officer on earth. And for the most vulnerable economies, the window to prevent a full-blown currency crisis is closing.

The Winners

The arithmetic of the oil exporters is straightforward. Brent crude above $100 a barrel generates revenues that exceed budget assumptions, strengthen current account positions, and create fiscal space that did not exist six months ago. Saudi Arabia, the UAE, and other Gulf producers with access to alternative export routes — the East-West Pipeline, the Habshan-Fujairah line, the Trans-Arabian Pipeline — have maintained significant output even as Hormuz traffic has collapsed. Their currencies, pegged to or closely managed against the dollar, have held firm.

Brazil, a major oil and agricultural exporter, has seen the real appreciate as commodity revenues surge. The country’s diversified export base — oil, soybeans, iron ore, beef — gives it natural protection against any single commodity shock, and the current environment has favored nearly every category. Russia, the world’s pariah exporter, has found willing buyers for its crude across Asia at prices well above its budget break-even, providing fiscal oxygen despite ongoing Western sanctions.

Even within Africa, the split is visible. Nigeria, despite being a major oil producer, has struggled because its refining capacity is insufficient to process its own crude — leaving it paradoxically dependent on imported refined products whose prices have surged. Angola and the Republic of Congo, by contrast, have seen modest currency relief as oil revenues outpace the costs of the crisis.

The Losers

The importing nations are where the damage is concentrated. Pakistan, which imports virtually all of its oil and gas and a substantial share of its fertilizer, represents perhaps the most acute case. The rupee has weakened sharply, foreign exchange reserves have been depleted by emergency energy purchases, and inflation — already elevated before the war — has accelerated to the point where the central bank faces an impossible choice between defending the currency and supporting an economy that is barely growing.

Bangladesh faces a similar predicament. The country’s garment-export-driven economy depends on imported energy to power its factories and imported fertilizer to feed its agricultural sector. The taka has come under sustained pressure, and the current account deficit has widened. Sri Lanka, which was already recovering from its 2022 economic collapse, has seen hard-won macroeconomic stability threatened by energy import costs that its treasury cannot easily absorb.

Vietnam, which had been one of the fastest-growing economies in Southeast Asia and a magnet for foreign direct investment, is discovering the vulnerability that rapid industrialization creates when energy dependence outpaces domestic production. The dong has weakened, and the State Bank of Vietnam has been forced to intervene in currency markets while simultaneously managing inflation expectations.

India occupies a unique middle ground. As the world’s third-largest oil importer, it is acutely vulnerable to the Hormuz disruption. The rupee has depreciated modestly — a managed outcome that reflects the Reserve Bank of India’s substantial foreign exchange reserves and its willingness to deploy them. But the cost is real. The government has raised export duties on diesel and aviation fuel to preserve domestic supply. LPG shortages have disrupted household cooking across millions of homes. And the bilateral energy deals being signed with the UAE, Russia, and other suppliers represent emergency measures, not permanent solutions.

The Reserve Burn

For the most vulnerable economies, the defining metric is the rate at which foreign exchange reserves are being depleted. Currency defense requires selling dollars and buying the local currency — a strategy that works only as long as the central bank has dollars to sell. Pakistan’s reserves, which were already at minimal levels, are being drawn down at a rate that external creditors are watching with growing alarm. Bangladesh’s reserve position, while stronger than Pakistan’s, offers less than six months of import cover at current prices — below the threshold that ratings agencies consider adequate.

The IMF has increased lending to several of the most affected economies, and the World Bank has accelerated disbursements from existing facilities. But multilateral support operates on timelines that do not always match the speed of currency crises. The gap between approval and disbursement, between commitment and cash, can be measured in weeks or months — an eternity for a finance ministry watching its reserves decline by hundreds of millions of dollars per week.

The risk is not hypothetical. Currency crises in importing nations tend to follow a predictable sequence: energy import costs widen the trade deficit; the current account deteriorates; reserves fall; the central bank raises interest rates to defend the currency; higher rates compress domestic demand; growth slows; capital flight accelerates; and the currency breaks through whatever level the central bank was defending. The speed of the sequence varies, but the logic is consistent. And for several countries in South Asia and sub-Saharan Africa, the early stages of this sequence are already underway.

The Fertilizer Channel

What makes this crisis particularly dangerous for emerging market currencies is that the pressure is not limited to energy. The fertilizer disruption — driven by the same Hormuz closure that has constrained oil and gas flows — is creating a second channel of inflation that operates on agricultural time rather than energy market time.

Countries that import nitrogen fertilizer from the Gulf are facing a double hit: higher fuel costs and higher input costs for the crops that feed their populations. The UN World Food Programme’s projection of 45 million additional people facing acute hunger is concentrated overwhelmingly in the developing world — in the same countries whose currencies are under the most pressure and whose governments have the least fiscal space to provide relief.

When food prices rise in economies where food constitutes 30 to 50 percent of household spending — as it does across much of South Asia and Africa — the currency impact is both direct and indirect. Direct, because higher food import bills worsen the trade balance. Indirect, because food inflation erodes real incomes, reduces consumer spending, weakens growth, and ultimately undermines the macroeconomic fundamentals on which currency stability depends.

The Policy Response

Central banks in the most affected economies face an unenviable toolkit. Raising interest rates can slow the currency’s decline but does nothing to address the supply-side nature of the inflation — and risks crushing domestic demand in economies that are already fragile. Allowing the currency to depreciate reduces the reserve drain but amplifies imported inflation, creating a feedback loop that is difficult to break. Capital controls can slow outflows but damage investor confidence and cut off the foreign investment that many of these economies depend on for growth.

The honest assessment is that there is no clean solution. The Hormuz crisis is a supply shock imposed on the developing world by a conflict in which most of these countries have no involvement and over which they have no influence. Their currencies are weakening not because of domestic policy failures — though in some cases those exist — but because the global commodity infrastructure on which they depend has been weaponized by belligerents who have no regard for the downstream consequences.

The BRICS framework, the bilateral swap lines that China has extended across Asia and Africa, the IMF’s rapid financing instruments, and the regional stabilization funds that have been discussed at every G20 meeting for the past decade — all of these were designed, in theory, for exactly this kind of moment. Whether they prove sufficient, and whether they arrive in time, will determine whether the Hormuz crisis remains a manageable disruption for the developing world or becomes something far worse: a synchronised currency crisis that pushes the most vulnerable economies past the point of recovery.

The currencies are already rendering their verdict. The question is whether anyone is listening.