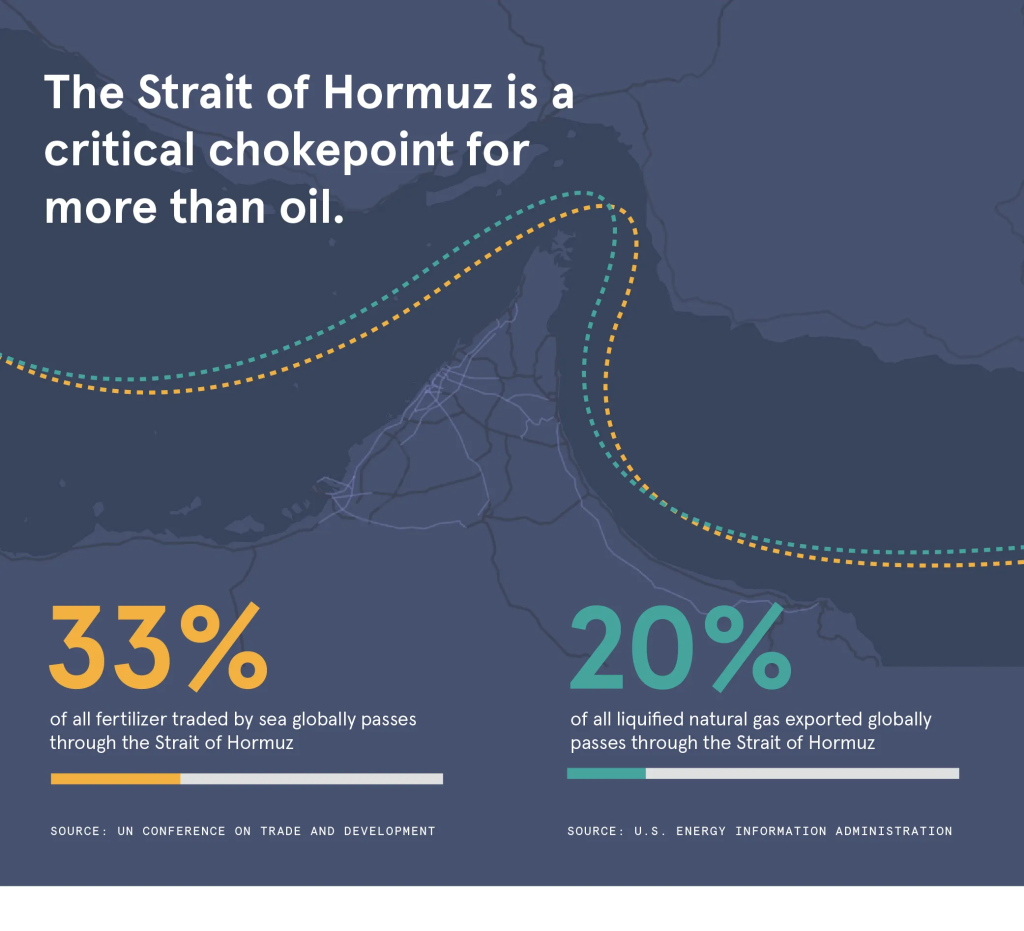

A third of globally traded fertilizer passes through the Strait of Hormuz. The Strait has been closed for nearly three months. Nitrogen prices have doubled. And the planting window that determines whether a billion people eat next year is already closing.

By The Index Today Staff · May 20, 2026 · Commodities · 10 min read

In January, nitrogen fertilizer cost $350 a ton. Today it costs $600. The price has not risen because of a hurricane, or a drought, or a currency collapse, or any of the familiar agricultural supply shocks that periodically disrupt food markets. It has risen because of a naval blockade in a strait 7,000 miles from the American Midwest, a war that most farmers couldn’t have located on a map six months ago, and a chain of consequences so long and tangled that it connects an Iranian Revolutionary Guard commander’s threat to “set ships ablaze” to the cost of corn on the cob at a summer barbecue.

The fertilizer crisis of 2026 is, in some ways, the most consequential dimension of the Hormuz disruption — more consequential, perhaps, than the oil shock that has dominated headlines. Oil prices surge and recede with every ceasefire rumor and diplomatic overture. Fertilizer is different. It operates on agricultural time, not news-cycle time. The nitrogen you fail to apply to soil in March and April cannot be compensated for in June or July. The crop yield you lose this spring does not come back next year. The food price inflation that results arrives months after the disruption that caused it, long after the world’s attention has moved on.

This is the crisis that the United Nations World Food Programme warned could push 45 million additional people into acute hunger. It is happening in slow motion, and it is already too late to fully prevent.

The Hormuz Bottleneck

More than one-third of globally traded fertilizer passes through the Strait of Hormuz. The countries surrounding the Persian Gulf — Iran, Saudi Arabia, Qatar, the UAE, Kuwait, Oman — collectively account for nearly 49 percent of global urea exports and about 30 percent of global ammonia exports. Urea is the most widely used nitrogen fertilizer on earth. It is the chemical input that determines, more than any other single factor, how much wheat, rice, corn, and soybeans the world produces in a given year.

Natural gas accounts for roughly 70 percent of the total production cost of nitrogen fertilizers. The Gulf is one of the world’s cheapest sources of natural gas. The combination of abundant feedstock and proximity to shipping lanes made the region the global center of fertilizer production — an arrangement that was efficient, profitable, and, it turns out, catastrophically fragile.

When Iran declared the Strait closed on March 4, the disruption was immediate. Tankers carrying urea, ammonia, and sulfur were stranded or rerouted. QatarEnergy declared force majeure. Sulfur exports — the Gulf accounts for roughly 45 percent of global supply — collapsed, sending sulfuric acid prices sharply higher and cascading through the phosphate fertilizer chain. Data from Kpler shows the scale of Asian dependence on the region: 35 percent of urea, 53 percent of sulfur, and 64 percent of ammonia exports flow to Asian buyers. Those flows stopped.

In the United States, some fertilizer prices rose more than 40 percent in a single month. Globally, the International Fertilizer Association’s data showed average prices tracking toward 15 to 20 percent above pre-war levels in the first half of 2026. For American farmers operating on already thin margins, the increase was painful but survivable. For smallholder farmers in South Asia and sub-Saharan Africa — the populations most vulnerable to food price inflation — it was potentially devastating.

The Planting Window

What makes this crisis different from the 2022 fertilizer spike triggered by Russia’s invasion of Ukraine is timing. The Hormuz closure coincided precisely with the Northern Hemisphere’s spring planting season — the narrow window during which farmers across North America, Europe, Russia, China, and India apply the fertilizer that will determine their yields for the entire year.

Cereal plants absorb the vast majority of their nitrogen during early growth. There is no catching up. Reducing nitrogen application by 10 to 15 percent, or delaying it by two to four weeks, can reduce corn yields by 10 to 25 percent. The decision that an Iowa corn farmer makes in April about how much fertilizer to apply is a decision that will shape global grain prices in September.

Francisco Martin-Rayo, CEO of agricultural prediction platform Helios AI, described the dynamic as a “domino effect” — higher input costs lead to lower fertilizer use, which leads to weaker yields, which leads to shrinking global grain stockpiles. “The fertilizer that you’re not putting into your crops in March and April, you can’t make up for in June and July if a ceasefire comes through,” he said. The damage, in other words, is already locked in.

The FAO’s chief economist, Maximo Torero, echoed the warning. If the conflict lasts beyond 40 days and input costs remain elevated, he said, farmers may reduce inputs, plant less, or switch to less fertilizer-intensive crops such as legumes. “Those choices will hit future yields and shape our food supply and commodity prices for the rest of this year and all of the next.”

The conflict has now lasted nearly three months.

The Global Ripple

The consequences are not evenly distributed. Markets entered 2026 with relatively high stocks of basic food commodities — a buffer that has cushioned the initial impact. Global cereal prices rose 1.5 percent in March, led by a 4.3 percent increase in wheat driven by worsening U.S. crop prospects and expectations of lower Australian plantings due to fertilizer costs. These are not panic numbers. But they are early numbers, and the trajectory points in one direction.

The FAO Food Price Index rose 2.4 percent from its revised February level. Vegetable oil prices climbed 5.1 percent — the third consecutive monthly increase. Rice prices, notably, fell 3 percent due to harvest timing and weaker import demand, providing temporary relief for the staple that feeds more people than any other grain. But rice is less nitrogen-dependent than corn or wheat, meaning the relative reprieve may not last as the broader food system adjusts to higher input costs.

The most acute vulnerability lies in countries that import both fertilizer and food: nations in sub-Saharan Africa, South Asia, and parts of Southeast Asia where agriculture is labor-intensive, fertilizer application rates are already below optimal levels, and household budgets cannot absorb food price increases without real human suffering. The UN World Food Programme’s estimate — 45 million additional people facing acute hunger if oil remains above $100 and the Strait remains closed through June — is not a projection about commodity markets. It is a projection about human beings who will not have enough to eat.

The Longer Shadow

Even if the Strait reopened tomorrow — and there is no indication it will — the agricultural consequences of the past three months are already baked into the 2026 growing season. The nitrogen that was not applied cannot be retroactively delivered to crops that needed it weeks ago. The planting decisions that were deferred or downscaled will produce less grain, less feed, less of everything that a global food system operating at the margin of sufficiency requires.

A smaller 2026 crop, with rising demand for livestock feed in China and India, will pressure global corn and wheat prices through the second half of the year and into 2027. Meat prices will follow, as feed costs are passed through to consumers. Processed food, which relies on corn-derived inputs at virtually every stage of production, will reflect the increase in ways that most consumers will experience at the supermarket without understanding the cause.

The comparison to 2022 is instructive but incomplete. When Russia invaded Ukraine, both agricultural commodity prices and fertilizer prices rose simultaneously — a double shock that was severe but at least partly self-correcting, as high crop prices incentivized continued production despite elevated input costs. This time, fertilizer prices have surged while crop prices have risen only modestly, compressing margins rather than expanding them. The incentive structure is worse, not better.

The deeper lesson is about concentration and fragility. The global food system’s dependence on a single maritime chokepoint for a third of its fertilizer supply was a known risk that no one prioritized until the risk materialized. The Strait of Hormuz was always a vulnerability. It was just never tested at this scale, at this moment in the agricultural calendar, with this many people depending on the outcome.

The war in Iran will end. The Strait will eventually reopen. But the crops that were underfertilized this spring will produce what they produce. The yields that were lost are lost. And the food prices that result will be paid — disproportionately, as always — by the people who can least afford them.